Instagram is growing its value faster than any other brand

The bulk of this year’s fastest risers in the BrandZ ranking come from the technology sector, while automotive and mass personal care brands struggle to keep pace.

A wide variety of brands with diverse marketing approaches are rising up in this year’s global BrandZ ranking of the top 100 brands by Kantar, showing that any sector or category is ripe for disruption.

A wide variety of brands with diverse marketing approaches are rising up in this year’s global BrandZ ranking of the top 100 brands by Kantar, showing that any sector or category is ripe for disruption.

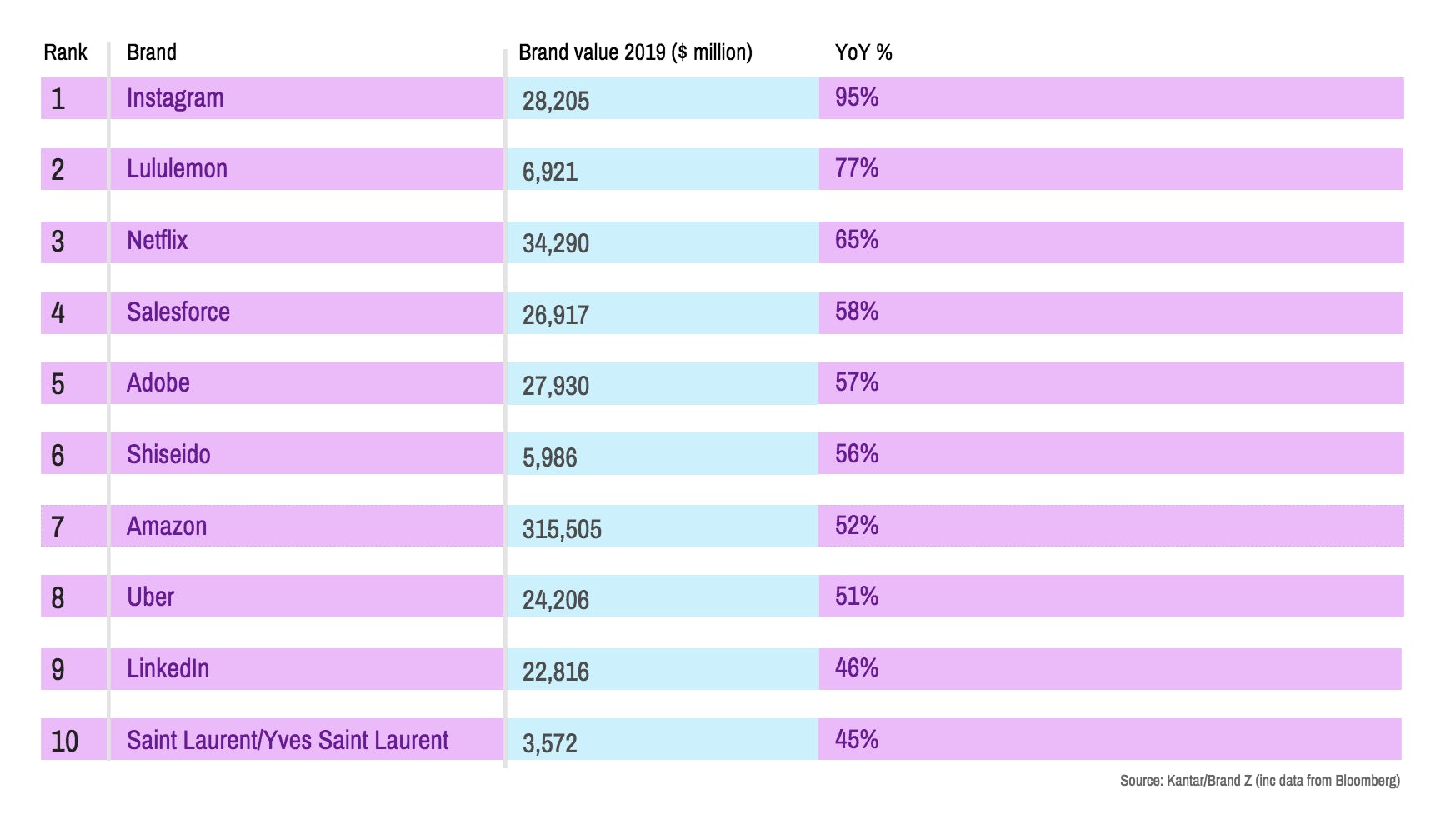

Facebook-owned Instagram is this year’s fastest riser, climbing 47 places after a 95% increase in brand value takes it to $2.82bn.

The second-fastest riser is Lululemon (77%) followed by Netflix (65%), Salesforce (58%), Adobe (57%) and Shiseido (56%).

READ MORE: Amazon beats Apple and Google to become the world’s most valuable brand

All of these brands have grown at a faster rate than this year’s leader Amazon, which increased its value by 52%. Other fast risers include Uber (51%), LinkedIn (46%), YSL (45%) and restaurant chain Chipotle (40%).

“Some [brands] are still establishing themselves, growing by reaching previously unexposed audiences, such as Instagram. Some are reminding consumers of what they stand for like Chipotle, or refreshing their positioning and perceptions like YSL,” explains Graham Staplehurst, BrandZ’s global strategy director.

“Others are extending and innovating into new sectors, as we are seeing with Uber expanding into home food delivery with Uber Eats and even underwater ride hailing ScUber on the Great Barrier Reef.”

He adds: “Many of the fastest growing brands are tapping into evolving consumer ecosystems, or are creating their own, like newcomers Meituan (78th) and Didi Chuxing (71st) in China. They are brands that keep themselves relevant to consumers and easy to choose and use.”

Due to an increased focus on lifestyle and wellbeing, luxury brands are having somewhat of a renaissance and are the fastest growing category this year (29%). Alongside YSL, top performances come from Dior (29%), Louis Vuitton (15%), Gucci (13%) and Hermes (10%).

Luxury is driving growth in the premiumisation of the personal care category too, with high-end personal care brands (Clinique, Estée Lauder, Garnier, Lancôme, L’Oréal, Shiseido) up 14% collectively, while mass personal care brands (Colgate, Crest, Dove, Gillette, Head & Shoulders, Nivea, Olay, Oral-B, Pantene) are down 4%.

READ MORE: How brands can grow in a volatile marketing world

Retail is the second fastest growing category (25%), and the strategies of the highest performers – including Amazon, Home Depot, Walmart, Costco, Ikea, Lowe’s and Aldi – indicate that if brands move with changing consumer needs and behaviours to deliver high quality experiences they can still win in a challenging retail landscape.

Of course, not all brands are growing in value. After Tencent, the biggest losers are GE (-32%), Baidu (-22%) and DHL (-19%), with other value-declining brands including Zara (-16%), Marlboro (-12%), IBM (-11%), Samsung (-6%) and Gillette (-8%).

Not one car brand increased its value in 2019, with BMW and Mercedes-Benz both down 9% and Toyota down 3%, while Ford and Honda drop out of the ranking completely. Meanwhile, with a brand valuation of $9bn, Tesla is close to entering the ranking for the first time.

Methodology

Kantar’s BrandZ valuation process takes the financial value created by a brand in US dollars and multiplies it by the proportion of that value generated by the brand contribution alone.

That brand contribution is derived from consumer research that quantifies how much of the volume people purchase and how much of the price premium people pay can be attributed to brand equity, connecting what people think to what they do.

This year’s analysis involves 122,000 brands, 3.6 million consumers, 418 categories, 51 markets and 5.1 billion data points.